2022 (end of year)

changes

As I have come to do every year, I’m sharing a few scattered thoughts that I’m thinking about as the year concludes.

Venture

Maybe it was the Macro all along.

“It seems to me that a significant portion of all the money investors made over this period resulted from the tailwind generated by the massive drop in interest rates.” — Howard Marks, Sea Change

I’ve always found the “macro” environment to be abstract and fairly uninteresting. Concepts like interest rates, inflation, and government policy are far less interesting to me than specific technology applications and products. Despite that, this year the macro has dominated the narrative. Inflation is high enough that you notice it at the grocery store and interest rates climbed quickly enough that home prices are out of whack. In years like 2022, it’s clear that “the macro matters” but it likely always has. I think in part, we’re less eager to point out that we benefitted from long-lasting, secular tailwinds. The next few years will be interesting as startups and public tech companies are valued under a new framework.

The decline of valuation-centric venture.

Valuations were a measure of success…We’re still trying to find our sober equilibrium. We are not there yet but I see signs of sobriety and a new generation of startups who never had access to the Kool Aid.

— Mark Suster, Praying to the God of Valuation

In the past couple years, the term “founder-friendly” became associated with high valuations and fast term sheets. The best product you could provide founders was centered around the deal rather than the following years of partnership. This was a natural byproduct of a frothy fundraising environment. If your next capital raise wasn’t going to be all that challenging, then you might as well optimize for dilution now. As we head into a more “normal” fundraising environment, I think priorities will shift. I tend to view this as a net positive that should yield more large successful businesses even if those businesses are built more slowly.

______

World

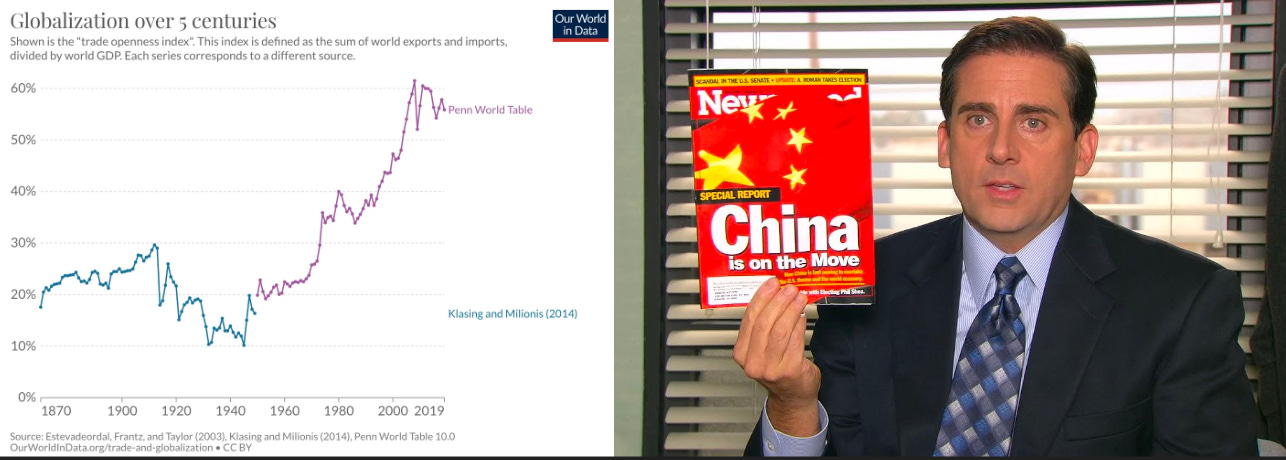

The reversal of globalization.

“Globalization is almost dead and free trade is almost dead. A lot of people still wish they would come back, but I don't think they will be back.”

— Morris Chang, CEO of TSMC

The post-WW2 era has seen the explosion of globalization and free trade. In the period that followed, air transport, ocean freight, and global communication costs came down dramatically leading to much more global supply chains. This megatrend is plateauing in the face of the pandemic, geopolitical tensions, and rising nationalist sentiment. I firmly believe that the world has improved over time and will continue to do so. If we look back, much of the improvements in our daily lives are a result of the cost arbitrage of making goods cheaper elsewhere. What happens when those benefits plateau?

Leverage in software-driven business models.

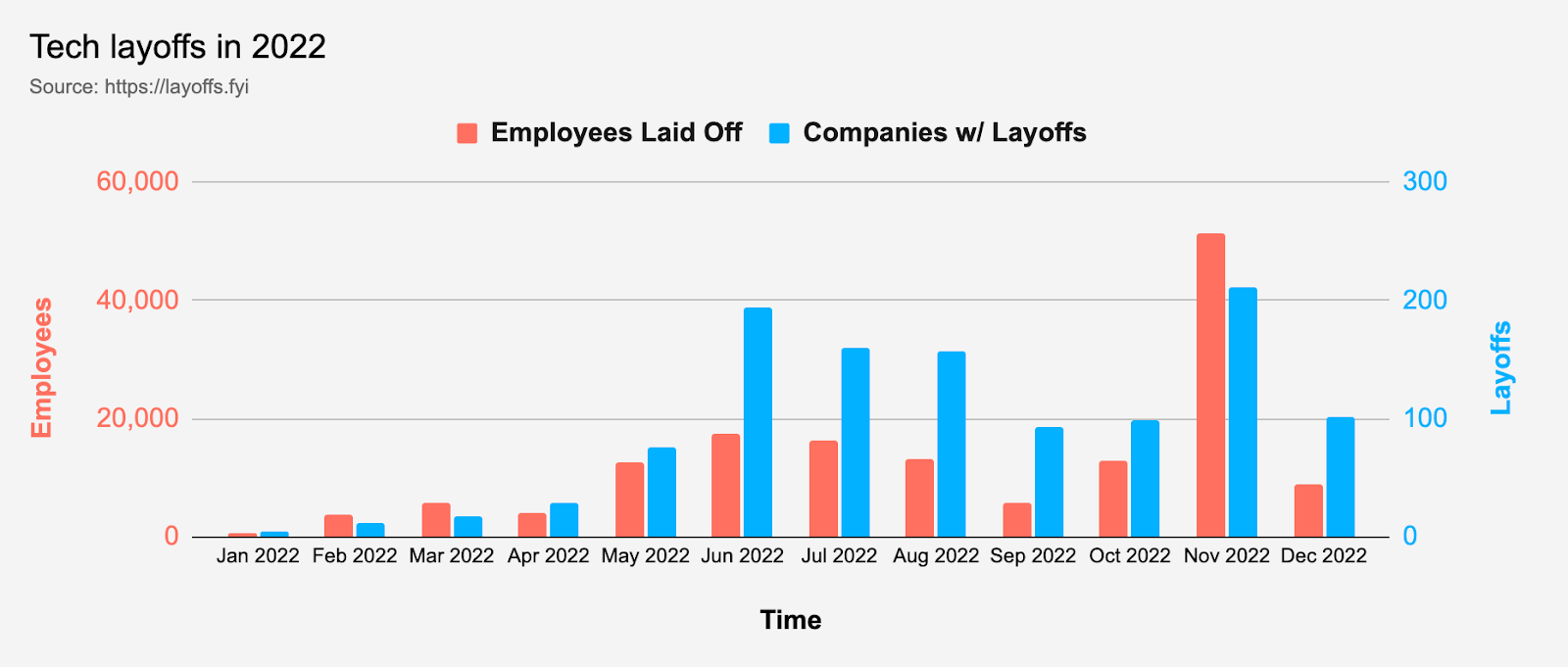

As valuations fell, companies were forced to bring down expenses in order to push towards profitability. This forced tech companies to cut thousands of jobs driven by companies like Twitter, aggressively cutting most of their headcount. It feels like every company has tried to tell the story of how it will 10x and consequently, aggressively hired to pursue these new growth opportunities. As the market turns and capital becomes more expensive, more companies will realize they are better off trying to be an efficient, cash-generating business rather than overinvest in hopes of becoming the next FAANG-like business. I think Twitter is one of these such businesses.

It feels to me that the whole idea of software being an extremely high leverage business model has come into question. There are examples like WhatsApp, operating at extreme efficiency with only 55 employees at the time of their $19B acquisition. But large tech companies have added headcount at alarming rates. Facebook reported its first-ever decline in revenue this year, but at the same time they have still grown significantly in the past few years.

I think both the private and public markets have been generous with the timelines they expect companies to get to profitability. Companies like Uber and Lyft are still grappling with making their unit economics work despite being around for over a decade. I think these types of companies with very unproven economics will have a more challenging time to raise.

Personal

On a more personal note, this was a year of some exciting changes for me. I married my best friend over the summer and am grateful to have had a beautiful celebration surrounded by family and friends. A few months later, we moved from the Bay Area to New York. There’s definitely a bit of culture shock, but the energy of New York is intoxicating and am excited to call this place home.

Life is good. Happy Holidays!